Technology One (ASX:TNE) stock is up 6.1% over the past three months. Since the market usually pays for a company’s long-term financial health, we decided to examine its fundamentals to see if they could affect the market. Specifically, we decided to examine Technology One’s ROE in this article.

Return on equity, or ROE, is a key measure used to assess how efficiently a company’s management is using the company’s capital. In short, ROE shows the profit generated by each dollar relative to the investment of its shareholders.

Check out our latest analysis on Technology One

How do you calculate return on equity?

Return on equity can be calculated using the formula:

Return on equity = Net income (from continuing operations) ÷ Equity

So, based on the above formula, the ROE for Technology One is:

34% = A$103 million ÷ A$306 million (Based on trailing twelve months to September 2023).

“Return” is the amount earned after tax in the last twelve months. Another way to think about it is that for every AUD$1 of equity, the company has managed to earn AUD$0.34 in profit.

What is the relationship between ROE and revenue growth?

We have already established that ROE serves as an effective profit-generating measure of a company’s future earnings. Now we need to estimate how much profit the company is reinvesting or “holding back” for future growth, which then gives us an idea of the company’s growth potential. Assuming everything else remains the same, the higher the ROE and earnings retention, the higher the growth rate of a company compared to companies that do not necessarily carry these characteristics.

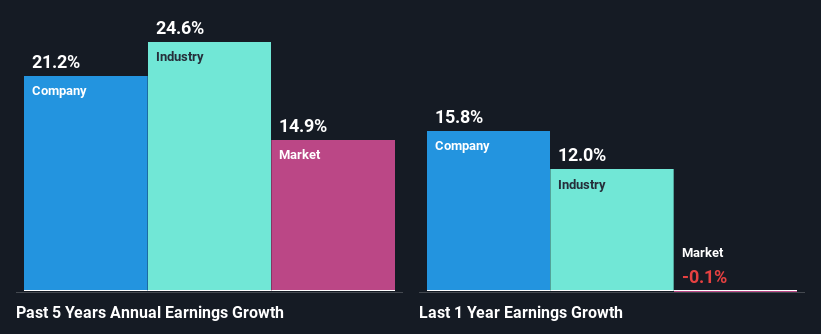

Side by side comparison of Technology One’s earnings growth and 34% ROE

First, we recognize that Technology One has a significantly high ROE. Second, even compared to the industry average of 9.5%, the company’s return on equity is quite impressive. As a result, Technology One’s extraordinary 21% net income growth over the past five years is no surprise.

Next, comparing Technology One’s net income growth to the industry, we found that the company’s reported growth is similar to the industry average growth rate of 25% over the past few years.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is whether the expected earnings growth or lack thereof is already built into the stock price. This will help them determine whether the future of the stock looks promising or ominous. If you’re wondering about Technology One’s valuation, check out this price-to-earnings ratio benchmark against its industry.

Is the technology using its retained earnings effectively?

The high three-year average payout ratio of 59% (meaning it retains just 41% of earnings) for Technology One suggests that the company’s growth hasn’t really been hindered, even though it has returned most of its earnings to its shareholders.

In addition, Technology One is committed to continuing to share its profits with shareholders, which we infer from its long history of paying dividends for at least ten years. Our latest analyst data shows that the company’s future payout ratio over the next three years is expected to be approximately 56%. Therefore, the company’s future ROE is also not expected to change much, with analysts forecasting an ROE of 33%.

Summary

Overall, we are quite pleased with the performance of the Technology One. Especially the high ROE that contributed to the impressive growth seen in revenue. Although the company reinvested only a small portion of its profits, it still managed to increase its revenue, so it is tangible. With that said, the latest forecasts from industry analysts reveal that the company’s revenue growth is expected to slow. Are these analyst expectations based on general industry expectations or the company’s fundamentals? Click here to be taken to our analyst’s forecast page for the company.

Have feedback on this article? Concerned about content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article from Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts, using only an unbiased methodology, and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell shares and does not take into account your goals or your financial situation. We aim to provide you with long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or quality materials. Simply Wall St has no position in the stocks mentioned.