I was looking at the BLS data after last week’s inflation announcement, and one number stuck out like Victor Wembanyana standing next to a group of kindergarteners.

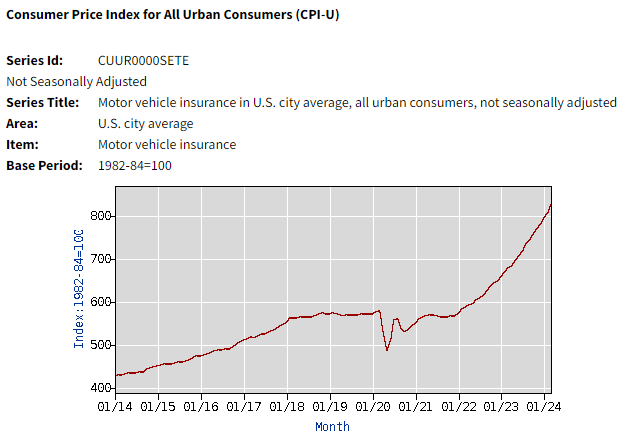

Motor insurance has grown by 22% over the previous 12 months against an overall inflation rate of 3.5%. Check out the change in car insurance prices over the past few years:

It’s like meme stock.

Since the start of 2020, car insurance has jumped 46% amid an overall CPI increase of nearly 22%:

Most of the increase has come recently.

So what’s going on here? Why is car insurance rising so much faster than the average basket of prices?

I did some research and talked to a handful of people in the insurance space. It’s not just one thing. Here are the main reasons as far as I can tell:

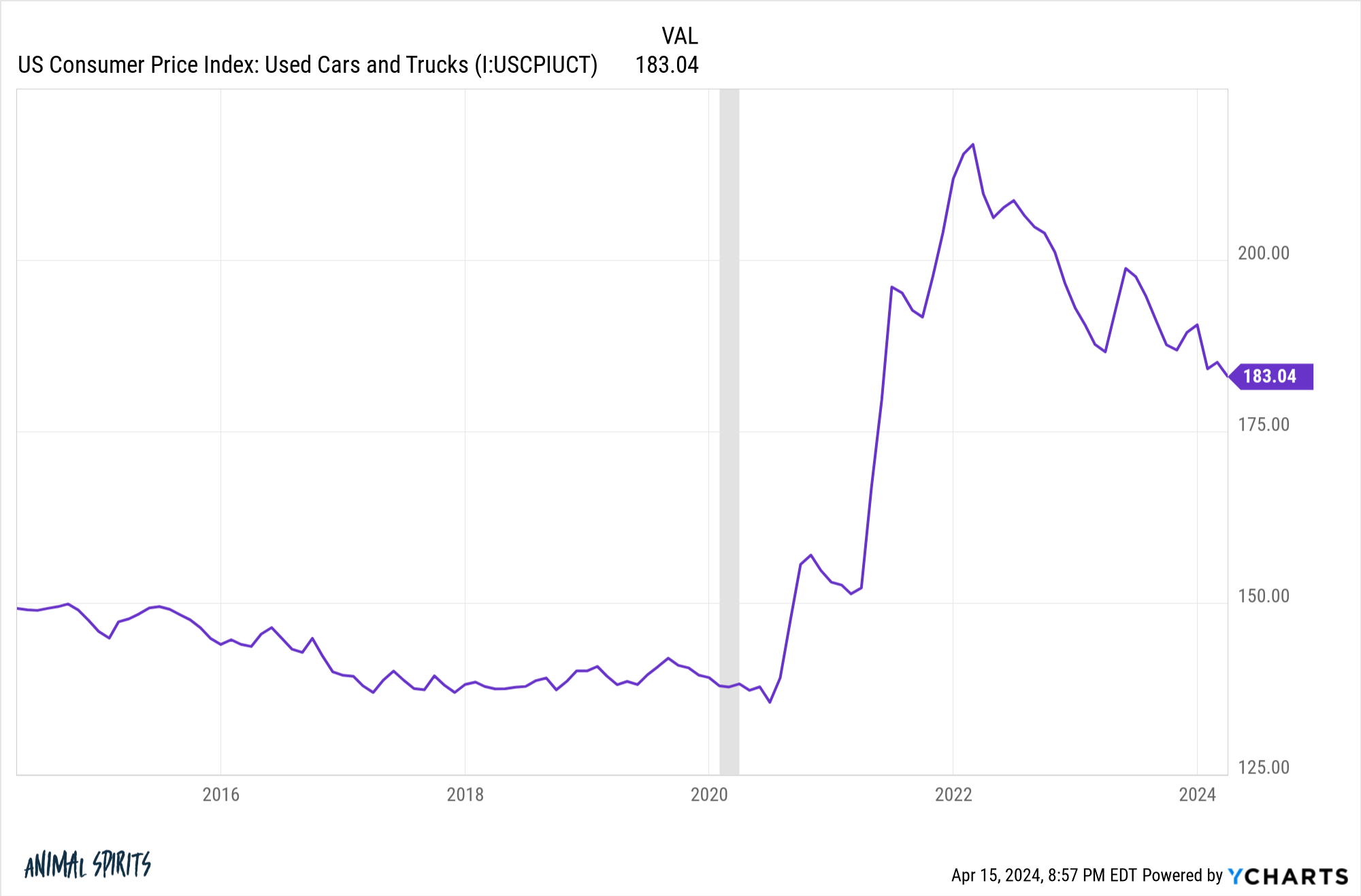

Car prices are higher. Replacement costs for other vehicles have risen a lot during the pandemic. Just look at the rising prices of used cars:

There were pandemic and supply chain reasons for this, but more expensive vehicles mean higher replacement costs, which means higher insurance premiums.

People also drive bigger and more expensive vehicles these days, which increases costs.

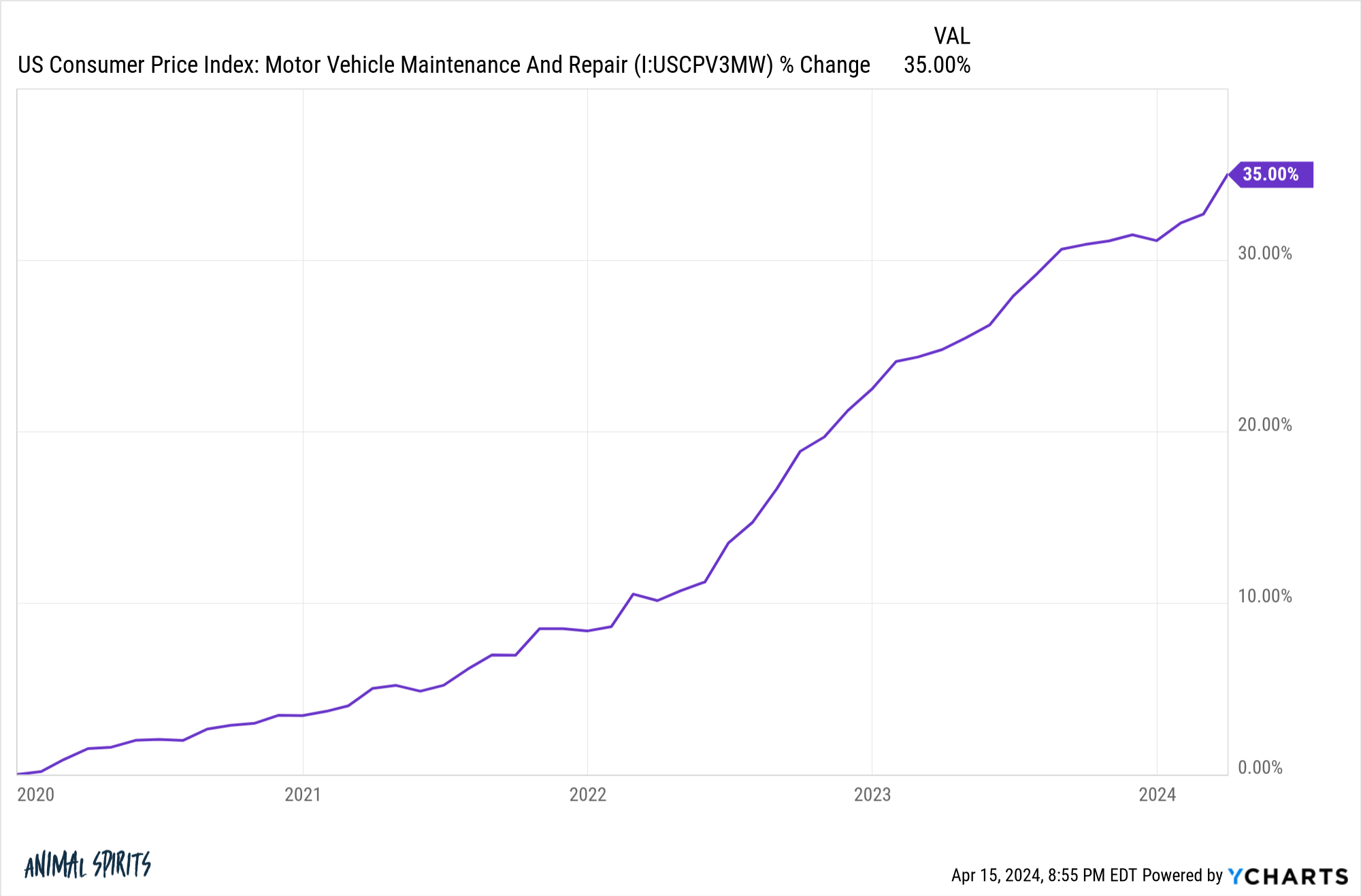

Support and parts. A few years ago I ran into a small fender flare with my Explorer. All it needed was a new rear bumper and some new panels. It was still driveable.

Total repair costs were more than $15,000 (all I paid was my deductible).

Supply chains didn’t help. But all the new sensors, technology and cameras meant parts were much more expensive and work more complicated.

More complicated work and inflation in parts prices also translate into increased repair labor costs.

This helps explain why inflation is so much higher in these areas:

With the advent of electric cars and self-driving vehicles, this will become even more expensive.

Drivers are getting worse. People started driving faster and more recklessly during the pandemic with fewer cars on the road. This behavior did not stop after traffic returned.

Plus, the combination of larger trucks and SUVs, along with increased smartphone use while driving, has led to the highest level of pedestrian deaths in 40 years.

People staring at their phones while driving is like adding drunk drivers to the roads at any time of the day.

With more accidents come bigger insurance claims.

Climate change. Nearly 360,000 cars were destroyed or damaged during Hurricane Ian.

Hurricanes, wildfires and other natural disasters make car insurance more expensive. Some people in climate-affected areas see more limited insurance options. Some insurers are pulling out of these areas altogether.

It’s not just car insurance. The Wall Street Journal recently ran a story on property insurance increases:

The average annual cost of home insurance has increased by about 20% between 2021 and 2023 to $2,377, according to insurance shopping site Insurify, which predicts another 6% increase in 2024.

Worst of all, home insurance premiums are rising. Rates rose an average of more than 10% in 19 states in 2023 after a series of large payouts related to floods, storms, wildfires and other natural disasters in the U.S., according to an Insurance Information Institute analysis of data from S&P Global Market Intelligence. More Americans have also moved to disaster-prone areas in recent years, increasing exposure to these events.

So even if you’ve already locked in the price of your house and car, these ancillary costs can still increase the cost of ownership.

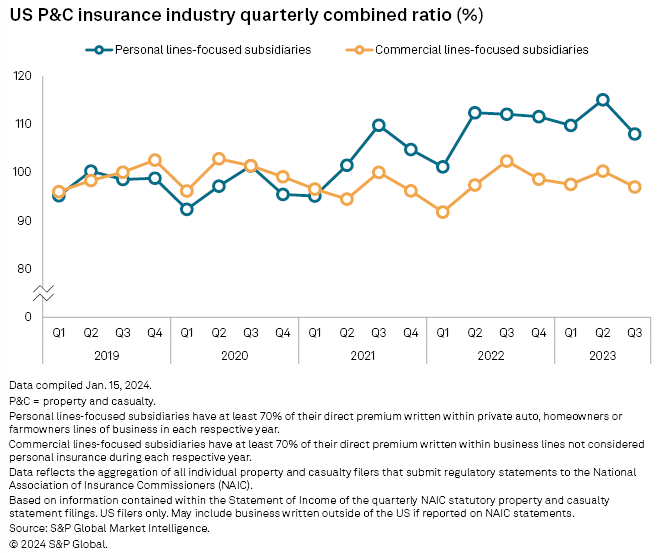

Some would point to corporate greed as the reason for the increased costs, but the numbers don’t bear that out.

The combined ratio is a way of measuring profitability in the insurance space. Essentially, it is the losses plus expenses incurred by an insurance company divided by the premiums earned. The higher the ratio, the worse the profitability for insurers.

If the number is greater than 100, it means that insurers are losing money by paying out more than they are taking in. If it is below 100, it means they are profitable.

Data from Standard & Poors shows that personal home and auto insurance providers have been losing money for several years:

Payouts exceed premiums earned by customers.

So what happens from here?

Used car prices are falling after dramatic repricing during the pandemic. Hopefully this will lead to lower prices and lower premiums now that supply chains have strengthened.

It is harder to see improvement in the other problem areas in the coming years.

We Americans love to drive massive trucks and SUVs. With new technologies, our vehicles are becoming more and more complex. Unless we ban smartphones while driving, I don’t see a path to a road full of better drivers until we have fully self-driving cars.

And natural disasters seem to be increasing in frequency and severity.1

It’s hard to imagine a scenario where insurance rates drop dramatically to the levels consumers are used to.

My only financial advice is to shop around when your insurance comes due and you see higher premiums.

And get used to paying higher insurance rates, especially in some states.

More information:

How much is this truck worth to you for $70,000

1A less severe hurricane and wildfire season would obviously help as well.