It can be described simply as a technology company, but the main money maker for A click (NYSE: SNAP) is its popular Snapchat app. And with 750 million people using Snapchat every month around the world, it’s fair to say the app is a huge success.

Snap monetizes this huge Snapchat user base by serving ads. Of its 750 million monthly users, over 400 million use it on average every day. And its user base is heavily concentrated in younger demographics. The management believes that this is a desirable target audience for advertisers, hence it believes that it can increase ad revenue in the long run.

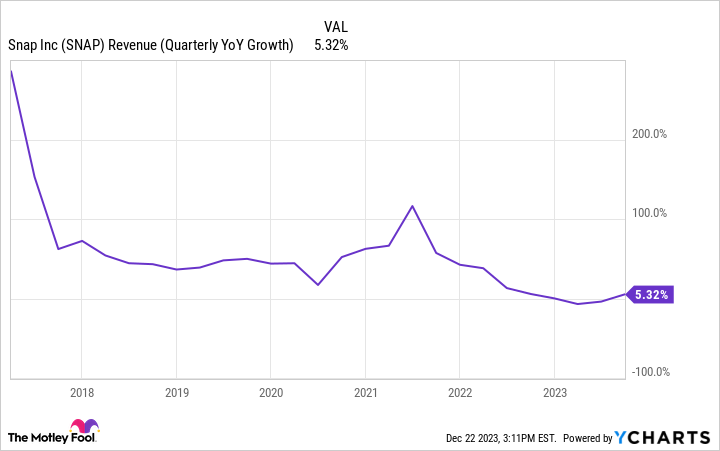

Recently, however, there has been a problem with this plan. Although Snap’s user base and ad impressions are growing, its ad revenue is struggling. In the third quarter of 2023, the company’s effective cost per thousand impressions (eCPM) — a measure of ad rates — declined 5% year-over-year.

Advertisers are not as willing to commit money in the current economic environment and therefore Snap is not growing as it used to, as the chart below shows.

In light of its ad revenue woes, Snap might just have hit on a business idea that will completely change its financials for the better. It’s a model that other successful companies have proven can work.

Snap’s $300 million new business

In mid-2022, Snap introduced a subscription tier for its Snapchat app. The service costs $3.99 per month and gives users access to additional features. And it’s growing like crazy.

In September, Snapchat+ had about 5 million subscribers — not bad considering it launched just over a year ago. But in December, the company said it now had 7 million subscribers. That’s about a 40% increase in less than three months.

At $3.99 per month, that puts Snapchat+ at an annualized rate of over $300 million. Therefore, with $4.5 billion in Snap’s total revenue over the past 12 months, Snapchat+ is already a significant revenue stream for the company.

In my opinion, Snap is following the model of other ad-based businesses such as Spotify and Duolingo. Both companies have discovered how much more powerful subscription revenue can be compared to ad-based free tiers.

For example, as of Q3 2023, Spotify has 574 million monthly active users, of which 226 million pay for an ad-free experience – just 39% of the user base. However, paying users accounted for a whopping 87% of revenue in the quarter.

For its part, Duolingo has the same dynamic. There are 83.1 million people using the language learning app on a monthly basis, but only 5.8 million paying users as of the end of Q3 2023. But subscription revenue is 77% of the total.

With both Spotify and Duolingo, only a small percentage of users pay, but those paying users represent the majority of the top line.

What to watch with Snap

Hypothetically, what would happen if only 5% of Snap’s user base started paying for Snapchat+? In that scenario, the company would pull in an impressive $1.8 billion in annual subscription revenue.

It’s easy to see how this could be a big deal for Snap, especially if its current rate of adoption remains strong in the coming quarters and years.

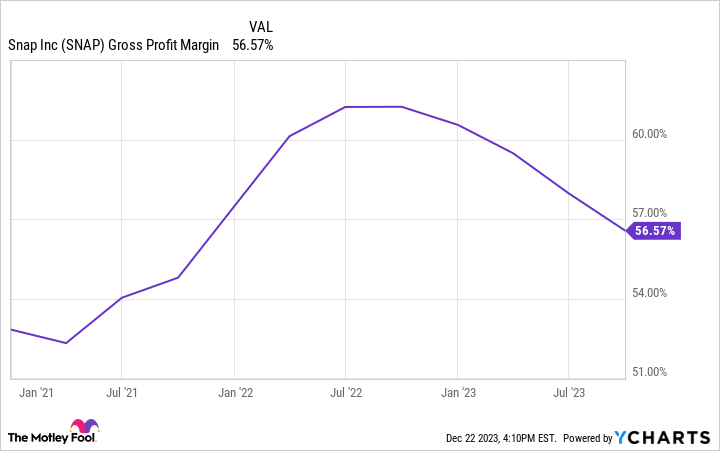

However, there is a catch in all this. Snap’s gross margin has been falling since the launch of Snapchat+, and that may be related.

In Q3, Snap’s infrastructure spending increased 51% year-over-year and 16% quarter-over-quarter. In short, the company’s investments in artificial intelligence (AI) and augmented reality (AR) come with increased costs. And some of the benefits of being a Snapchat+ subscriber are getting access to AI and AR tools.

Assuming the subscription tier takes off and Snapchat eventually gets infrastructure costs under control, this is something that could completely revolutionize Snap’s business. Revenue growth could jump as more users start paying, and Snap will avoid the ups and downs of the ad market.

It’s too early to tell whether or not this is a game changer for Snap. But the stock should definitely be on your watch list because the subscription level is something that can really improve the long-term outlook.

Should you invest $1,000 in Snap right now?

Before you buy Snap stock, consider the following:

The Motley Fool Stock Advisor the analyst team has just identified who they think they are 10 best stocks for investors to buy now… and Snap wasn’t one of them. The 10 stocks that made the cut could deliver monster returns in the coming years.

Stock advisor provides investors with an easy-to-follow blueprint for success, including portfolio construction guidance, regular analyst updates, and two new stock picks each month. The Stock advisor the service has more than tripled the return of the S&P 500 since 2002*.

Check out the 10 stocks

*Stock Advisor goes back to December 18, 2023

John Quast has no position in any of the stocks mentioned. The Motley Fool has positions and recommends Duolingo and Spotify Technology. The Motley Fool has a disclosure policy.

Snap has a brand new annual business of $300 million and is already up 40% since September, originally published by The Motley Fool