stock is a profitable investment bet")

Crocs, Inc. CROX looks well-positioned for growth thanks to its solid business strategies. The company benefits from robust consumer demand for the Crocs and HEYDUDE brands, supported by effective price action. Sees strength in clogs, sandals and customization for a while.

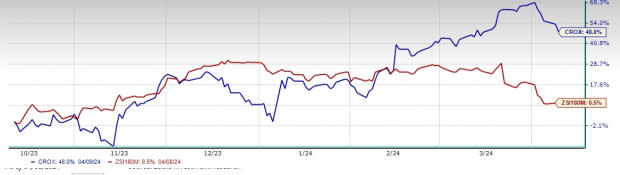

In the fourth quarter of 2023, the company’s bottom line beat the Zacks Consensus Estimate for the 15th time in a row. Buoyed by such gains, this current Zacks Rank #2 (Buy) company has gained 48% over the past three months, compared to 8.5% industry growth.

Let’s dig deeper

Crocs has been witnessing a decline in inbound transportation costs, which have been contributing to gross profits for quite some time now. In addition, favorable sea freight rates, lack of air freight and weaker promotional activity of the Crocs brand act as tailwinds. In the fourth quarter of 2023, adjusted gross profit rose 6.1% year-over-year, while adjusted gross margin increased 240 basis points (bps) to 55.7%, thanks to gains from lower costs of carriage of both brands.

Clogs, sandals, and personalization categories each saw double-digit growth in 2023. During the same period, the HEYDUDE brand generated revenue of nearly $950 million and more than $200 million in operating income. The company’s Jibbitz business has also been doing well for quite some time. This business grew 17% to more than $0.25 billion, representing approximately 9% of the total mix in 2023.

Image source: Zacks Investment Research

Management continues to view personalization as a mega-consumer trend, with the opportunity to expand Jibbitz’s penetration in 2024 through better wholesale execution, deeper international penetration and improved speed to market opportunities.

Crocs has previously outlined its long-term strategy and key initiatives to ensure sustainable growth. It was then expected to generate more than $5 billion in revenue by 2026, representing a compound annual growth rate of more than 17%.

It expects to achieve the revenue target driven by strong digital sales, improved market share for sandals, growth in Asia and innovative product and marketing. Management expects Sandal revenue to quadruple by 2026. The company targets at least 50% of total revenue to come from digital channels by the end of 2026. Driven by strong revenue growth, it forecasts improved profitability and cash flows by 2026.

In conclusion, Crocs seem like an attractive investment bet given all the aforementioned positives. Also, analysts seem quite bullish on the company. The Zacks Consensus Estimate for 2024 sales and earnings per share (EPS) are currently pegged at $4.1 billion and $12.38, implying growth of 3.9% and 2.9%, respectively, from year-ago levels . Consensus estimates for 2025 sales and EPS are currently pegged at $4.3 billion and $13.54, respectively, representing growth of 4.9% and 9.3%, respectively, over the prior year’s actuals. VGM’s A score further demonstrates strength.

Check out these solid photos too

Some other top ranked companies are Ralph Lauren RL, Royal Caribbean RCL and lululemon athletics LULU.

Ralph Lauren, a footwear and accessories retailer, currently holds a Zacks Rank #1 (Strong Buy). RL has an earnings surprise over the last four quarters of an average of 18.7%. You can see the full list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Ralph Lauren’s current fiscal year sales and EPS suggests growth of 2.7% and 22.7%, respectively, over the prior year’s figures.

Royal Caribbean currently carries a Zacks Rank #2. RCL has a profit surprise over the last four quarters of an average of 26.4%.

The Zacks Consensus Estimate for RCL’s 2024 sales and earnings per share point to increases of 14.7% and 47.9%, respectively, from year-ago levels.

lululemon athletica is an athletic apparel company inspired by yoga. LULU currently carries a Zacks Rank 2.

The Zacks Consensus Estimate for lululemon athletica’s current fiscal year sales and EPS suggests growth of 11.9% and 10.8%, respectively, over the prior year’s figures. LULU has a profit surprise for the last four quarters of an average of 9.7%.

Want the latest recommendations from Zacks Investment Research? Today you can download 7 best stocks for the next 30 days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Ralph Lauren Corporation (RL) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

To read this Zacks.com article, click here.

Zacks Investment Research