With its stock down 35% over the past three months, it’s easy to overlook UET United Electronic Technology ( ETR:CFC ). However, stock prices are usually determined by the company’s long-term financial performance, which in this case appears to be quite respectable. Specifically, we decided to examine UET United Electronic Technology’s ROE in this article.

ROE or return on equity is a useful tool for evaluating how effectively a company can generate a return on the investment it has received from its shareholders. In other words, it is a profitability ratio that measures the rate of return on the capital provided by the company’s shareholders.

Check out our latest analysis on UET United Electronic Technology

How to calculate return on equity?

The return on equity formula is:

Return on equity = Net income (from continuing operations) ÷ Equity

So, based on the above formula, the ROE for UET United Electronic Technology is:

76% = €3.8 million ÷ €5.0 million (Based on the last twelve months to June 2023).

“Return” is the annual profit. One way to conceptualize this is that for every €1 of shareholder equity it holds, the company makes €0.76 in profit.

Why is ROE important to earnings growth?

So far we have learned that ROE measures how efficiently a company generates its profits. Based on how much of its earnings the company chooses to reinvest or “hold,” we can then estimate the company’s future ability to generate earnings. Assuming everything else remains the same, the higher the ROE and earnings retention, the higher the growth rate of a company compared to companies that do not necessarily carry these characteristics.

UET United Electronic Technology’s revenue growth and 76% ROE

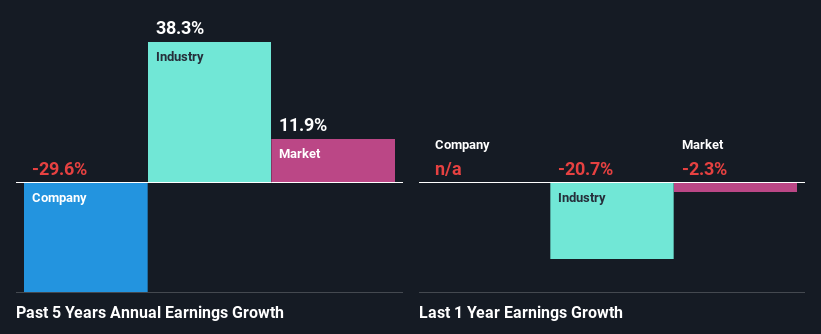

First, we recognize that UET United Electronic Technology has a significantly high ROE. Second, the comparison with the industry average ROE of 11% does not go unnoticed by us either. As you might expect, the 30% drop in net income reported by UET United Electronic Technology does not bode well for us. So there may be some other aspects that could explain this. For example, it could be that the company has a high payout ratio or the business has allocated capital poorly, for example.

So, as a next step, we compared UET United Electronic Technology’s performance to the industry and were disappointed to find that while the company has been shrinking its earnings, the industry has grown by 38% over the past few years.

Earnings growth is a huge factor in stock valuation. The investor should try to ascertain whether the expected growth or decline in profit, as the case may be, is included in the price. This will help them determine whether the future of the stock looks promising or ominous. If you’re wondering about UET United Electronic Technology’s valuation, check out this price-to-earnings ratio benchmark against its industry.

Is UET United Electronic Technology using its profits effectively?

Since UET United Electronic Technology does not pay any regular dividends, we conclude that it retains all of its earnings, which is quite confusing when you consider the fact that there is no earnings growth to show for it. So there could be other factors here that could potentially hamper growth. For example, the business faces some headwinds.

Summary

Overall, we think UET United Electronic Technology has some positive qualities. However, we are disappointed to see a lack of growth in earnings even despite a high ROE and high reinvestment rate. We believe that there may be some external factors that could have a negative impact on the business. While we won’t completely reject the company, what we would do is try to determine how risky the business is in order to make a more informed decision about the company. To learn the 4 risks we identified for UET United Electronic Technology, visit our risk dashboard for free.

Have feedback on this article? Concerned about content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article from Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts, using only an unbiased methodology, and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell shares and does not take into account your goals or your financial situation. We aim to provide you with long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or quality materials. Simply Wall St has no position in the stocks mentioned.